Stage as a label versus stage as an analytical input

Venture stage labels are used loosely. A "Seed" round can describe a pre-revenue company with a prototype, a business with $500k ARR and a defined go-to-market, or anything in between. The label alone says little about the risk being underwritten.

This matters because stage determines the base rates behind every assumption in a deal model. Survival probability, dilution path, realistic exit range: all of these move when the stage moves. Apply the wrong assumptions and the model breaks down quietly, producing numbers that look precise but rest on the wrong foundation.

One of the most visible symptoms is pitch decks built for the wrong round. A Pre-Seed company presents Series A metrics. A Seed company presents only vision. A Series A company still speaks in hypotheses instead of data. The mismatch is often apparent within the first few slides.

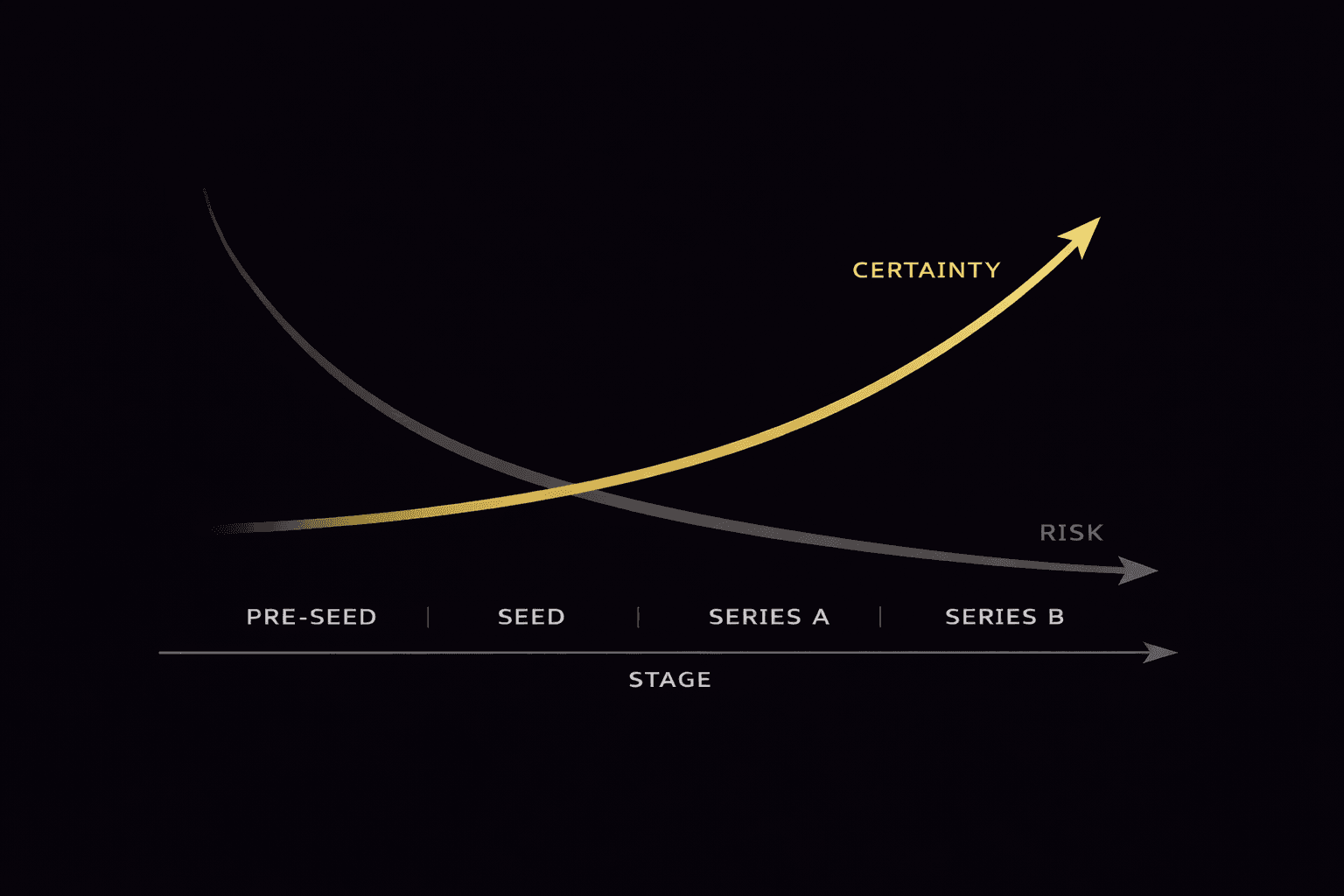

Stage is a risk category

The familiar alphabet progression (Seed, Series A, B, C) was not designed as a branding exercise. Each "Series" refers to a distinct class of preferred shares with its own rights and pricing. The Delaware C-Corp structure supports multiple share classes, and this legal flexibility likely contributed to how venture financing evolved. The precise historical origins are not well documented, but by the time institutional venture capital matured, the ecosystem had standardized milestone-based financing, with each round tied to a specific category of risk being reduced.

Over time, data providers such as PitchBook and NVCA helped formalise stage definitions based on revenue, traction, and funding size. Definitions vary by geography and sector, but the logic is the same everywhere. Revenue is a signal, not the definition. The critical investor question at any stage is: what uncertainty has already been removed?

| Stage | Primary risk being reduced |

|---|---|

| Pre-Seed | Team and build risk |

| Seed | Product-market fit risk |

| Series A | Scalability and repeatability risk |

| Series B | Market expansion and execution risk |

| Series C+ | Efficiency and exit readiness risk |

Pre-Seed: underwriting the team

At Pre-Seed, the company typically has a concept validated through research or early prototypes, an MVP under development or recently launched, and limited or no recurring revenue. Valuations are largely negotiated risk pricing. Data from AngelList and PitchBook suggests pre-money valuations in developed markets often cluster in the low single-digit millions (USD), depending on geography and sector.

Investors at this stage are underwriting people and insight. A fundable Pre-Seed deck needs to articulate a problem worth solving, a unique angle on that problem, and a market large enough to support venture returns. The founding team's capability and a clear roadmap to a Seed milestone matter more than financial projections. Use of funds should tie directly to risk reduction. Projections at this stage are directional at best. Execution credibility is what carries the round.

Seed: evidence of demand

By the Seed stage, the product is live. There are paying customers or early engagement signals, initial revenue, and the beginnings of a growth pattern. The core question has changed: not "can this be built?" but "do customers demonstrably want this?"

A fundable Seed deck balances narrative and data. Retention and early cohort behaviour carry more weight here than top-line revenue. Investors want to see whether acquisition has any repeatability to it: monthly growth rates, some clarity on the sales cycle, and cohort retention that is above noise level. Initial unit economics help, even if imperfect. The deck that works at this stage is the one that makes a credible case for predictable growth.

Series A: proving repeatability

Series A is a metrics-driven round. Companies at this stage typically have recurring revenue (in SaaS, often $1M+ ARR, though context matters), repeatable acquisition channels, and early evidence of scalable unit economics. The question investors are asking is whether growth can be systematically accelerated with capital.

The deck should make that case through numbers, not narrative. Revenue growth trajectory, cohort retention curves, gross margin stability, CAC payback, and LTV/CAC are all expected. A bottom-up financial model is standard. Cambridge Associates' research on venture performance dispersion shows that returns are power-law distributed, which means Series A investors are looking for outlier potential. If the metrics don't suggest it, the story alone won't carry the round.

Series B: scaling the engine

At Series B, the company has significant revenue (often $10M+ ARR in SaaS, sector dependent), demonstrated acquisition efficiency, and an emerging category position. The central question is execution at scale: can this organization capture a large share of its market?

Investors expect operational maturity at this stage. The deck should make the case through sales efficiency metrics, funnel analytics, gross margin durability, and a credible path to profitability or defensible market position. KPI dashboards matter more than product vision slides. If Pre-Seed decks are about the team and the insight, Series B decks are about the machine.

The most common error

Companies frequently raise money without clearly defining the milestone that the round must unlock. Each round should fund a specific transition. Pre-Seed to Seed means a product built with validated demand. Seed to Series A means a repeatable acquisition model. Series A to Series B means a scalable growth engine. Running out of runway between these milestones is one of the most common failure mechanisms in venture-backed companies.

The error is usually visible in the deck itself. A Pre-Seed deck overloaded with financial models signals inexperience. A Series A deck centred on storytelling without metrics signals opacity. Stage alignment shows up in how the deck is structured, not just what it claims.

How Auryn uses stage

Each stage in Auryn carries default assumptions set by the investment team, including target return multiples and baseline exit probabilities. When an analyst evaluates a deal, the company is measured against the expectations for its stage. When that company appears in the portfolio view, the same assumptions carry through.

Auryn also stores a snapshot of the assumptions at the time of investment, so the team can compare what they underwrote against where the company stands today. What you assumed at entry stays visible as the position evolves.

Want to continue the conversation?

Drop us a line if something here sparked an idea, or if you just want to talk.

Get in touch